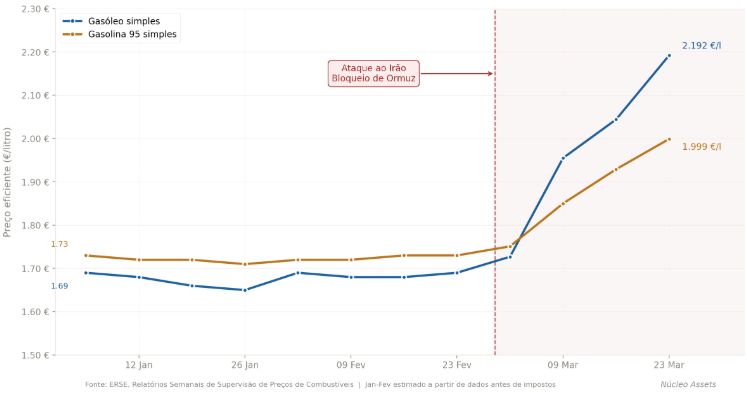

“Between late February and late March, the benchmark price of petrol rose by about 15%, and diesel by more than 25% (ERSE). Comparisons with 2022 are inevitable, but the conflict in Iran is very different from the war in Ukraine.

In 2022, the disruption hit materials directly. Ukraine supplied steel. Russia supplied the gas that powers cement, glass, and ceramics production. When those supply chains broke, construction material prices jumped nearly 16% year-on-year (INE). Energy, materials, and logistics were all hit at once, and the impact took months to show up in construction budgets.

The Strait of Hormuz disruption starts from a different place. The trigger is “only” energy: it affects around 20% of global oil supply. There’s no immediate shortage of materials from broken routes.

But there’s one variable linking the two scenarios: liquefied natural gas (LNG).

Europe receives a significant share of its LNG through the Strait, and entered this disruption with gas storage below 40% capacity, the lowest level in recent years. Gas is a key input for cement, glass, and ceramics, high-temperature industries that can’t easily electrify in the short term. If prices rise persistently, production costs will follow.

In Portugal, construction cost pressure has mainly come from labour (+9% year-on-year in 2024), while material costs have risen by less than 1%. This development could reopen a second front of pressure that had been largely dormant.

Market conditions add another layer of complexity. The Lisbon Metropolitan Area still faces more demand than supply. House prices rose nearly 18% year-on-year in Q3 2025 (INE), driven by demand. Reduced VAT on construction and renovation aims to boost supply, but a cost surge does the opposite: it undermines project viability.

The Bank of Portugal has already revised growth down from 2.3% to 1.8% and expects inflation at 2.8%.

The link between construction costs and sale prices isn’t linear: prices today are driven more by demand than by production costs. But when higher costs stall or kill new projects, future supply tightens, and with demand holding up, prices can only go one way.

The question isn’t whether this disruption will push up construction costs. It’s when, how much, and whether developers, builders, and investors have already priced it in.“

Source: ERSE, Relatórios Semanais de Supervisão de Preços dos Combustíveis (março de 2026); INE, Índice de Custos de Construção de Habitação Nova; INE, Índice de Preços da Habitação (T3 2025); Banco de Portugal, Boletim Económico (março de 2026); European Gas Hub; Bruegel, “How will the Iran conflict hit European energy markets”; Dezeen, “Construction material costs to rise with Strait of Hormuz blockade.

João Grilo via LinkedIn